{kind=link}

[ad_1]

I acquired an e mail from Vanguard notifying me of upcoming modifications to its charge schedule. The one change that stands out for me is that Vanguard might cost $100 efficient July 1 if I switch an account to a different dealer until I’ve $5 million with Vanguard.

I’ve been investing with Vanguard for over 25 years. I’ve had the sensation from some modifications by Vanguard in recent times that I’m not as valued as earlier than. This newest announcement lastly pushed me to the inevitable. I submitted a request to switch my account to Constancy earlier than the brand new charge takes impact.

When you’re considering alongside the identical strains, you must examine just a few issues earlier than you switch your accounts out of Vanguard. I’m not suggesting that everybody ought to go away Vanguard. This information is barely for many who intend to switch. It’ll make your switch from Vanguard go extra easily.

1. Do you have got a taxable account at Vanguard?

Tax-advantaged accounts equivalent to Conventional and Roth IRAs may be transferred to a different dealer with out tax penalties. The switch doesn’t generate a 1099 type. It doesn’t rely towards your annual contribution restrict. Please skip to Step 3 should you solely have tax-advantaged accounts at Vanguard.

Transferring a daily taxable brokerage account wants extra cautious consideration.

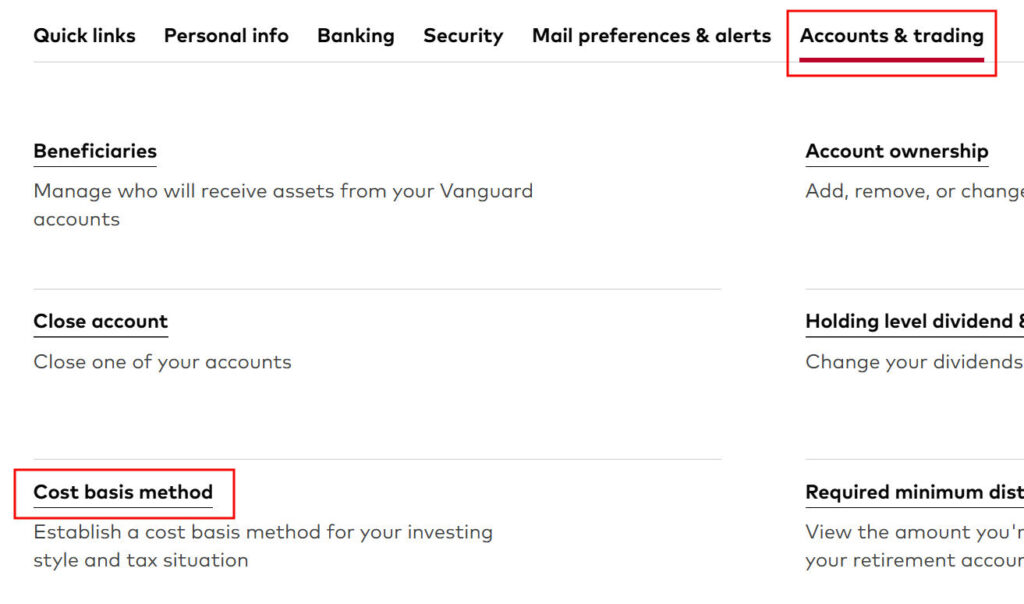

2. Value Foundation Methodology Election in Taxable Account

When you’ve got mutual funds (not shares, ETFs, bonds, or brokered CDs) in a daily taxable brokerage account, you must first ensure the price foundation methodology of your holdings is about to Particular Identification (“SpecId”). The default value foundation methodology for mutual funds is Common Value. Setting it to SpecId will switch the price foundation of every tax lot if you switch your account. It’ll allow you to reduce taxes if you promote sooner or later. If the price foundation methodology remains to be Common Value if you switch, solely the common value will switch to your receiving dealer and you’ll lose your buy historical past.

This solely applies to taxable accounts. You don’t must do something with the price foundation methodology in tax-advantaged accounts.

You may see or change your present setting in Profile & settings (the top icon) -> Accounts & buying and selling tab -> Value foundation methodology.

The change might take a day or two to finish. Wait till it’s completed earlier than you proceed.

3. Do you have got Vanguard mutual funds?

Particular person shares, ETFs, bonds, and brokered CDs are all equally out there at one other dealer. You may switch these simply to a different dealer and maintain, purchase, or promote them on the new dealer. Please skip to Step 5 should you solely have particular person shares, ETFs, bonds, and brokered CDs in your Vanguard account.

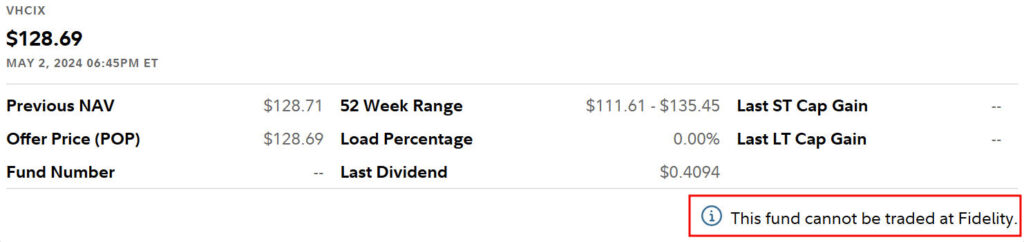

Not all Vanguard mutual funds may be held by all brokers outdoors of Vanguard. Please examine with the receiving dealer to see if they’ll settle for your Vanguard mutual funds. For instance, should you seek for VHCIX (Vanguard Well being Care Index Fund Admiral Shares) on Constancy’s web site, you’ll see a small be aware saying “This fund can’t be traded at Constancy.”

As Steve famous in remark #34, having this be aware doesn’t imply that Constancy can’t settle for it in a switch. Considered one of my funds has this be aware and it transferred efficiently.

In case your receiving dealer can settle for your Vanguard mutual funds, there’s often no cost for holding present shares or robotically reinvesting dividends however you’ll have to pay a fee if you purchase extra shares of these funds. Constancy and Charles Schwab don’t cost a fee for promoting shares of Vanguard mutual funds you already personal however they do cost for getting extra shares outdoors of computerized dividend reinvestments. Another brokers cost for each shopping for and promoting.

I’ve Vanguard mutual funds however I’m not shopping for new shares in these funds. I’ll solely maintain, robotically reinvest dividends, and promote my present shares over time. I gained’t incur any charges once I maintain my Vanguard mutual funds at Constancy.

4. Do your Vanguard mutual funds have ETF shares?

In case your receiving dealer can’t settle for your Vanguard mutual funds or if it could settle for them however you need to purchase extra shares sooner or later apart from robotically reinvesting dividends, see in case your funds are additionally out there as an ETF. Search for the fund on Vanguard’s web site. If the fund can be out there as an ETF, it’ll say so beneath the identify of the fund.

Vanguard can convert these mutual funds to the equal ETF tax-free with out a charge. You’ll must name Vanguard to transform them to ETF. After your funds are transformed to ETFs, you possibly can switch the ensuing ETFs to a different dealer and purchase extra shares of the ETFs on the new dealer.

For instance, Vanguard Well being Care Index Fund Admiral Shares (VHCIX) can be out there as Vanguard Well being Care ETF (VHT). You may switch the ETF and purchase extra shares after you change VHCIX to VHT.

Changing to ETF is an possibility however it isn’t at all times needed when the fund may be accepted by the receiving dealer. You may hold holding the Vanguard mutual funds and solely reinvest dividends and promote at Constancy or Schwab. If you should purchase extra shares, purchase an ETF or an alternate fund. You’ll have two holdings for a similar asset class however it’s not a giant deal.

There’s a small threat that the price foundation shall be tousled if you ask Vanguard to transform your mutual funds to ETFs in a taxable account. It shouldn’t occur however you by no means know. I didn’t need to take that likelihood once I transferred a taxable account from Vanguard. I don’t thoughts solely holding the Vanguard mutual funds, robotically reinvesting dividends, and promoting with out a fee at Constancy. I simply gained’t purchase new shares of these funds.

This small threat of messing up the price foundation doesn’t apply to tax-advantaged accounts. I’d convert eligible mutual funds to ETFs in a tax-advantaged account earlier than I switch.

When you resolve to transform your mutual funds to ETFs in a daily taxable brokerage account, remember to full Step 2 earlier than you name Vanguard. If a mutual fund remains to be on the Common Value methodology when it will get transformed, the transformed ETF will solely have the common value.

Some Vanguard funds aren’t out there as an ETF. When you switch your account, shopping for new shares of these funds will seemingly incur a fee on the new dealer. You’ll have to seek out another. Some Vanguard funds not out there as an ETF are nonetheless the very best of their class. For instance, Vanguard cash market funds and muni bond funds constantly have decrease bills and better yields than comparable Constancy or Schwab funds. Some retirees additionally just like the Vanguard Wellington and Wellesley funds. Possibly you must hold your account at Vanguard if you’ll purchase extra shares of these funds.

5. Put together the Receiving Account

When you resolve to switch however you don’t have already got an account of the identical sort on the receiving dealer, it’s higher to create one forward of time and configure it to the proper settings. The account sort ought to match (Conventional-to-Conventional, Roth-to-Roth, taxable-to-taxable). The account identify must also match (individual-to-individual, joint-to-joint, trust-to-trust). In the event that they don’t match, please repair them on both aspect first.

Some brokers pay a bonus for incoming transfers. It’s a must to enroll particularly for the bonus and have it coded to your account. I gained’t switch to a dealer just for the bonus however I’ll take the bonus if I already need to switch to that dealer and it occurs to pay a bonus. Please ask your assigned rep on the receiving dealer in case you have one.

Dividend reinvestment and value foundation monitoring methodology in your incoming switch will comply with the settings within the receiving account. Have a look and set them to your desire earlier than your investments are available in. The associated fee foundation monitoring methodology for mutual funds is about to Common Value by default in a brand new account. Change it to Precise Value, Recognized Value, or one thing to that impact for higher management over taxes in a taxable account. When you don’t change the setting away from Common Value, the price foundation of your incoming funds could also be recalculated to the common value.

I robotically reinvest dividends and use the default value foundation methodology in tax-advantaged accounts. In a taxable account, I robotically ship the dividends to the spending account and use Precise Value for the price foundation and Constancy’s Tax-Delicate lot disposal methodology. Charles Schwab calls them Recognized Value and Tax Lot Optimizer.

Beneficiary settings in your Vanguard account gained’t come over with the switch. Set your beneficiaries within the receiving account earlier than you switch.

6. Watch for Every thing to Settle

When you’ve got current transactions in your Vanguard account (cash in, cash out, trades, changing mutual funds to ETFs), you must anticipate every little thing to settle earlier than you switch your account. It’s simpler for everybody should you switch when nothing is within the air.

Don’t promote your investments to money forward of time earlier than you switch. Doing so in a taxable account will set off capital good points and taxes. Promoting in a tax-advantaged account will make you miss out on good points if the market occurs to surge whilst you anticipate the switch. Constancy and Schwab don’t cost for promoting Vanguard mutual funds after your switch is accomplished.

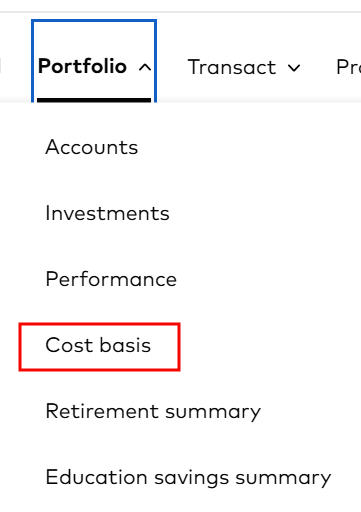

7. Save Value Foundation Particulars of Taxable Accounts

It’s essential to maintain the price foundation data correct if you switch a taxable account. You need to save or print your value foundation particulars in your Vanguard account earlier than you switch. This doesn’t apply to tax-advantaged accounts.

You see these particulars beneath Portfolio -> Value foundation.

Increase “Present lot particulars” beneath every holding. Save the web page to a PDF or print it.

8. Save Account Quantity and Latest Assertion

You’ll want to offer your Vanguard account quantity and a current assertion if you switch your account. The statements are beneath Exercise -> Statements.

The assertion doesn’t present your full account quantity. You have to copy your account quantity and reserve it individually.

9. Request Switch of Property on the Receiving Agency

You need to provoke the switch on the receiving agency. The method is often on-line. It’s beneath Accounts & Commerce -> Transfers after which “Transfer an account to Constancy” in Constancy. Search for one thing comparable at different brokers.

You’ll be requested the place you’re transferring from, the account quantity on the sending agency, what sort of account it’s, whether or not you’d prefer to switch every little thing within the account or solely a part of it, which account you’re transferring into, and eventually to connect a current account assertion of the supply account.

When you’re requested whether or not you’d prefer to switch in-kind or promote and switch money, ensure to decide on in-kind. In-kind means transferring every holding as-is with none change. Solely transferring in-kind gained’t set off taxes in a taxable account.

The switch often takes every week or sooner to finish. My switch accomplished in 4 enterprise days.

Many locations ship an alert if you log in from an “unknown gadget” nowadays however I didn’t hear something from Vanguard when my whole account went out of the door. Vanguard didn’t ship any affirmation or alert once they acquired the switch request to stop fraud. Nor did they ship any warm-hearted parting message to probably welcome me again sooner or later or any exit survey to ask the place they might’ve completed higher. It shattered all my phantasm that I used to be a valued buyer/proprietor.

10. Confirm Value Foundation in Taxable Account

If the switch is profitable, the holdings will come over first with out the price foundation particulars. That’s regular. Vanguard will ship the price foundation particulars in one other week or two. You need to confirm the price foundation particulars in opposition to the data you saved in Step 7.

11. Residual Sweep

When you do a full account switch and any of your investments pays dividends or curiosity throughout or after the switch, the dividends and curiosity should go into your outdated account. There shall be one other computerized sweep to switch any residual quantities. You don’t should provoke it. It’ll come over in just a few weeks.

12. 1099 Varieties Subsequent Yr

Your Vanguard login nonetheless works after you switch your account. You’ll nonetheless get the 1099 varieties subsequent yr from Vanguard for any actions that occurred earlier than the switch. Set a calendar reminder to obtain the 1099 varieties from Vanguard subsequent yr.

***

Transferring a Vanguard account isn’t tough however it requires some planning, particularly if you’re transferring a taxable account with mutual funds. Typically it’s higher to not switch. A very powerful elements are to not promote something and set off taxes and to protect the price foundation data for particular person heaps in taxable accounts.

Say No To Administration Charges

In case you are paying an advisor a share of your belongings, you might be paying 5-10x an excessive amount of. Discover ways to discover an unbiased advisor, pay for recommendation, and solely the recommendation.

[ad_2]