[ad_1]

The earlier submit Backdoor Roth in TurboTax: Recharacterize and Convert, 1st Yr handled contributing to a Conventional IRA for the earlier 12 months and recharacterizing a earlier 12 months’s Roth IRA contribution as a Conventional IRA contribution. This submit handles the conversion half.

Right here’s the primary instance situation:

You contributed $6,500 to a Conventional IRA for 2022 in 2023. The worth elevated to $6,700 once you transformed it to Roth in 2023.

You already reported the contribution half in your 2022 tax return. The IRA custodian despatched you a 1099-R kind for the conversion in 2023. This submit reveals you the right way to put it into TurboTax.

Right here’s the second instance situation:

You contributed $6,500 to a Roth IRA for 2022 in 2022. You realized that your earnings was too excessive once you did your 2022 taxes in 2023. You recharacterized the Roth contribution for 2022 as a Conventional contribution earlier than April 15, 2023. The IRA custodian moved $6,600 out of your Roth IRA to your Conventional IRA as a result of your unique $6,500 contribution had some earnings. The worth elevated once more to $6,700 once you transformed it to Roth in 2023.

You already reported the recharacterized contribution in your 2022 tax return. The IRA custodian despatched you two 1099-R types, one for the recharacterization, and the opposite for the conversion. This submit reveals you the right way to put each of them into TurboTax.

For those who contributed for 2023 in 2024 or for those who recharacterized a 2023 contribution in 2024, you’re nonetheless within the first 12 months of this journey. Please comply with Backdoor Roth in TurboTax: Recharacterize and Convert, 1st Yr.

If neither of those instance eventualities suits you, please seek the advice of our information for a standard “clear” backdoor Roth: How To Report Backdoor Roth In TurboTax (Up to date).

Use TurboTax Obtain

The screenshots under are from TurboTax Deluxe downloaded software program. The downloaded software program is approach higher than on-line software program. For those who haven’t paid to your TurboTax On-line submitting but, you should purchase TurboTax obtain from Amazon, Costco, Walmart, and plenty of different locations and swap from TurboTax On-line to TurboTax obtain (see directions for the right way to make the swap from TurboTax).

1099-R for Recharacterization

This part solely applies to the second instance situation. For those who didn’t recharacterize (the primary instance situation), please skip this part and bounce over to the conversion part.

We deal with the 1099-R kind for recharacterization first. This 1099-R kind has a code ‘R’ in Field 7.

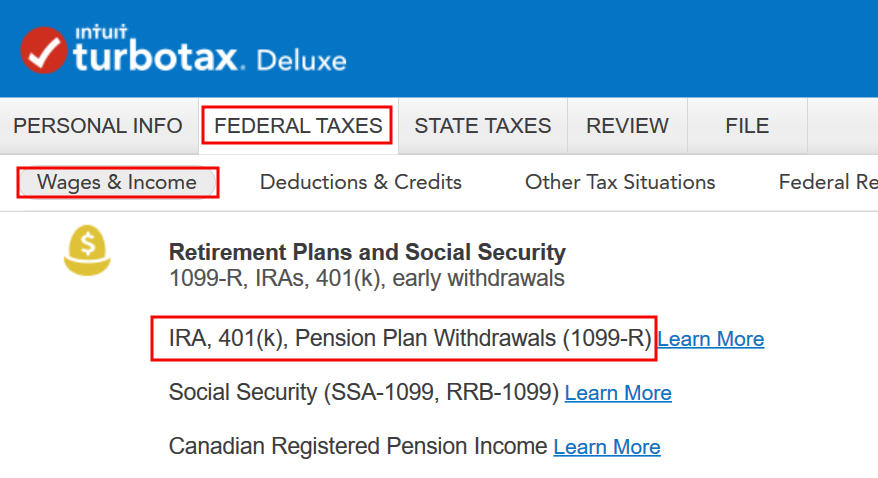

Go to Federal Taxes -> Wages & Earnings -> IRA, 401(ok), Pension Plan Withdrawals (1099-R).

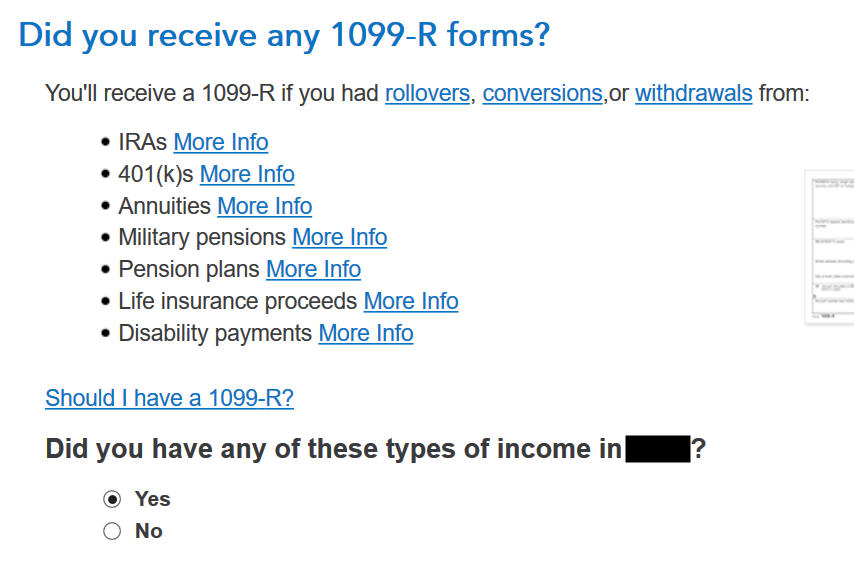

Affirm that you’ve got acquired a 1099-R kind. Import the 1099-R for those who’d like. I’m selecting to kind it myself.

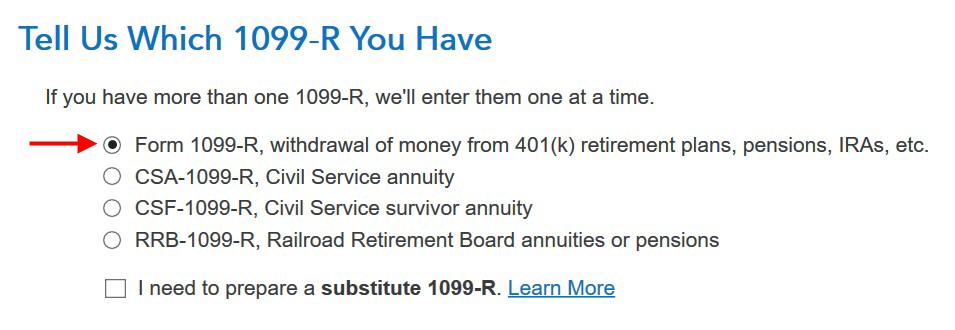

It’s an everyday 1099-R.

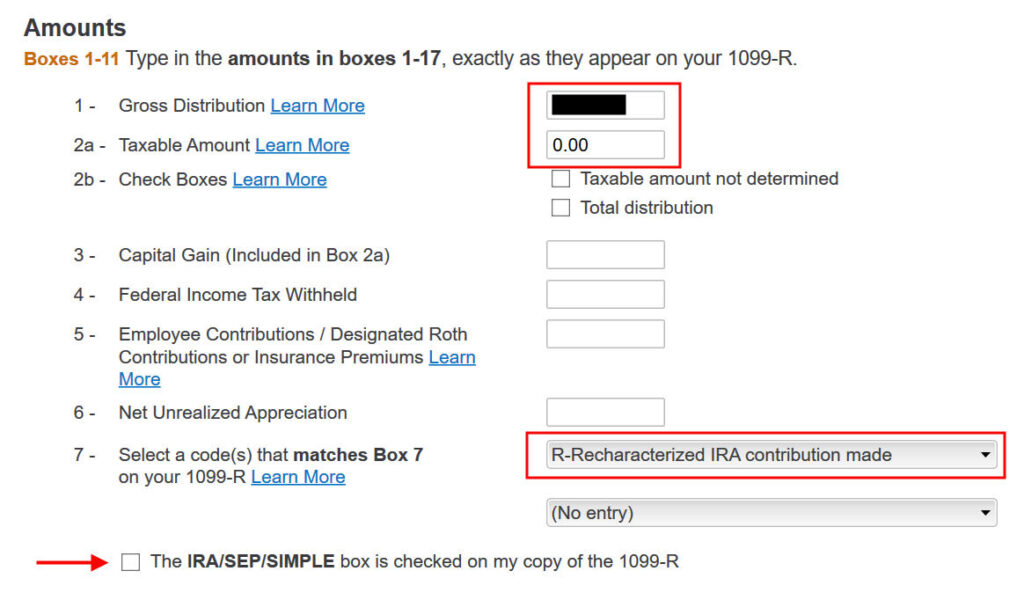

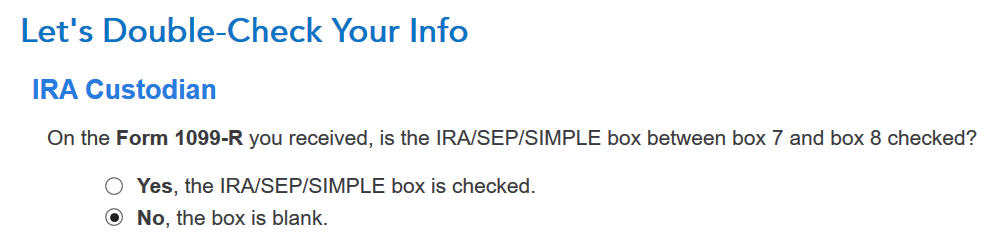

The quantity that moved out of your Roth IRA to your Conventional IRA reveals in Field 1. The taxable quantity in Field 2a is zero. The 2 checkboxes in Field 2b aren’t checked. The code in Field 7 is “R.” The “IRA/SEP/SIMPLE” field below Field 7 could or will not be checked. It’s not checked in our pattern 1099-R.

That field is clean in our 1099-R, and that’s OK.

It’s regular to see zero in Field 2a and clean in Field 2b. TurboTax simply desires to double-check.

Not a Public Security Officer.

If you’re doing taxes for 2023, chances are high the 1099-R kind is for 2023. Click on on the button that matches the 12 months on the shape.

No Must Amend

That is deceptive. You already reported the recharacterization within the earlier 12 months’s tax return for those who adopted our earlier submit. You solely must amend your earlier tax return for those who didn’t comply with these steps.

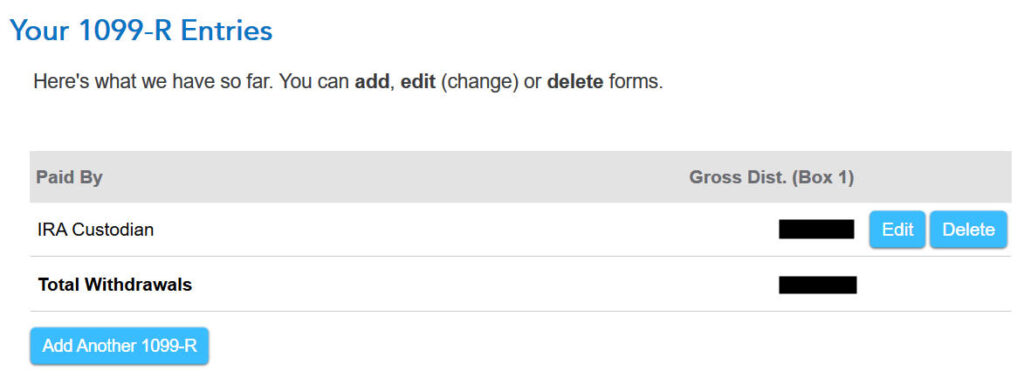

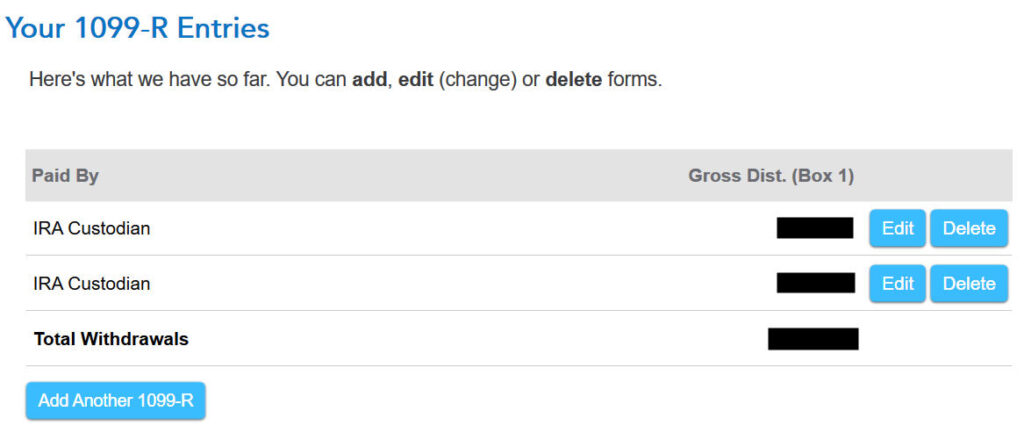

You’re achieved with the primary 1099-R kind. Click on on “Add One other 1099-R” so as to add the second for those who don’t have already got each 1099-R types imported.

1099-R for Conversion

The second 1099-R kind can also be an everyday 1099-R.

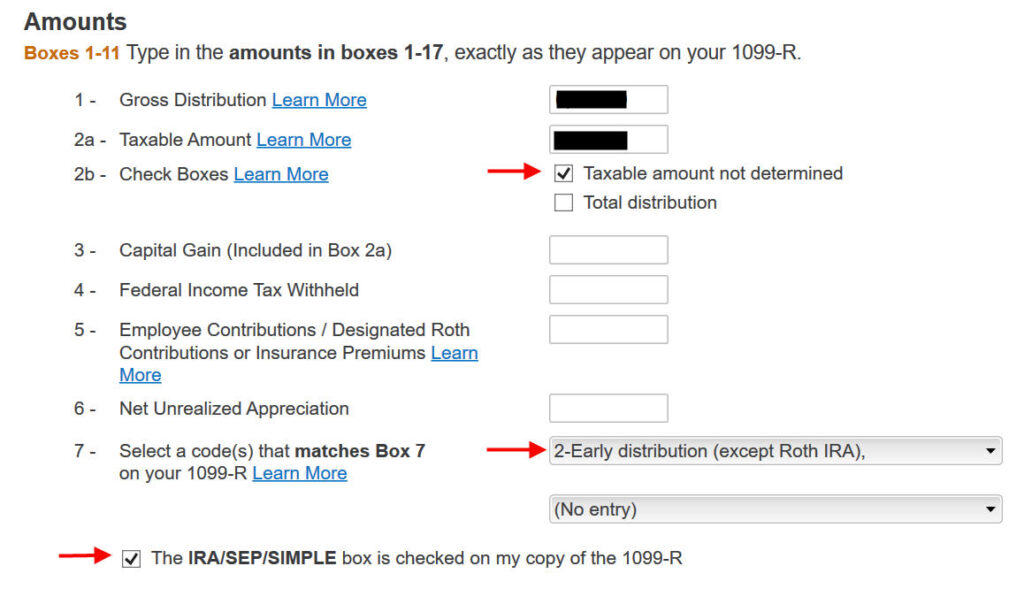

It’s regular to see the conversion reported in Field 2a because the taxable quantity when Field 2b is checked to say “Taxable quantity not decided.” The code in Field 7 is ‘2’ once you’re below 59-1/2. It’s ‘7’ once you’re over 59-1/2. The “IRA/SEP/SIMPLE” field is checked on this 1099-R kind for the conversion.

It says that you just don’t owe additional tax on this cash. In case your refund meter drops, don’t panic. It’s regular and short-term.

It’s not a Roth SIMPLE or a Roth SEP.

Didn’t inherit it.

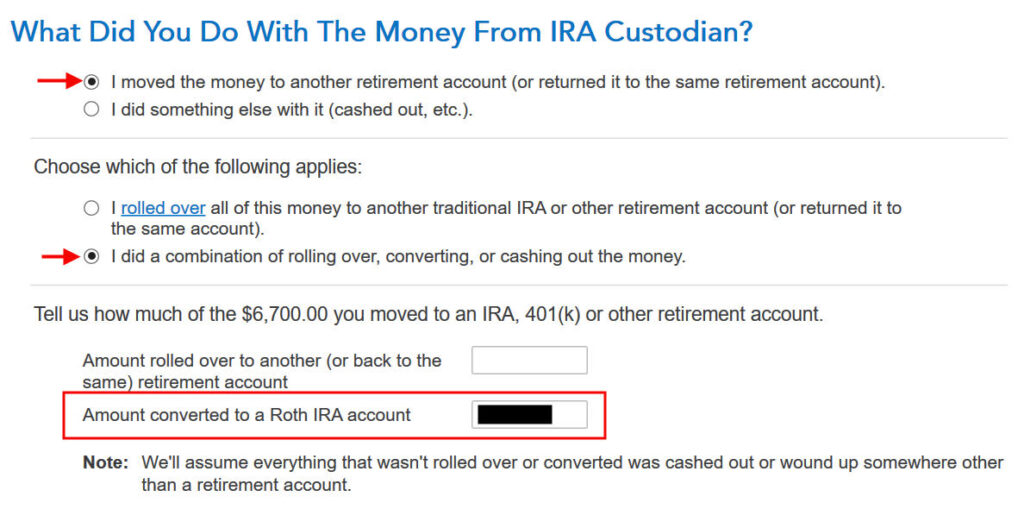

Transformed

First click on on “I moved …” then click on on “I did a mix …” Enter the quantity you transformed to Roth within the field. Don’t select the “I rolled over …” possibility. A rollover means Conventional-to-Conventional. Changing to Roth isn’t a rollover.

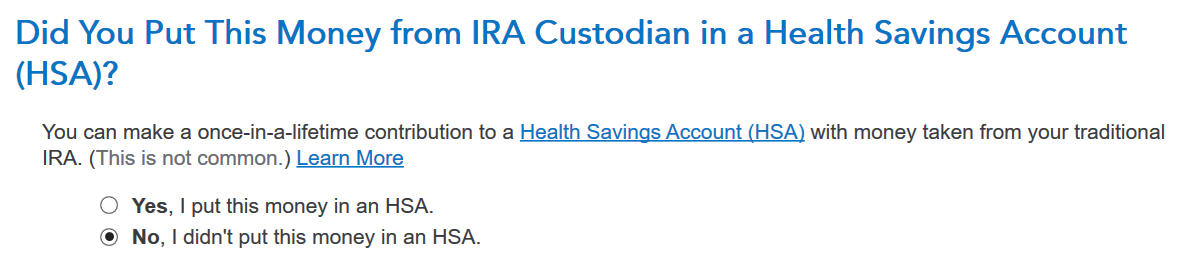

Didn’t put it in an HSA.

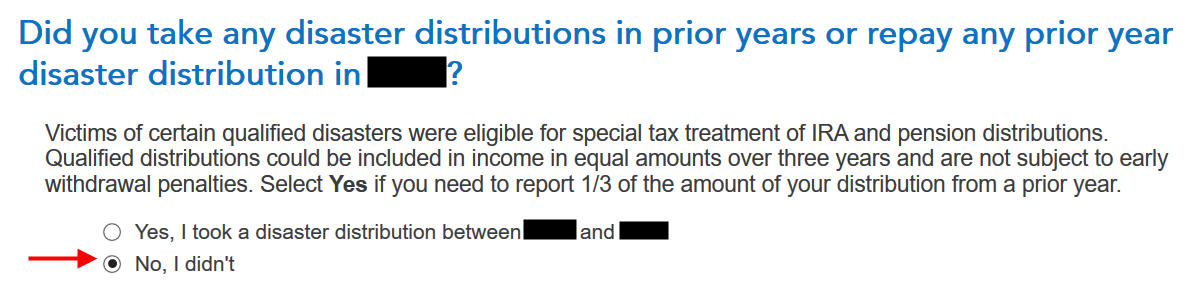

Not as a consequence of a catastrophe.

Now the 1099-R abstract contains each 1099-R types. Maintain going by clicking on “Proceed.”

No catastrophe distributions.

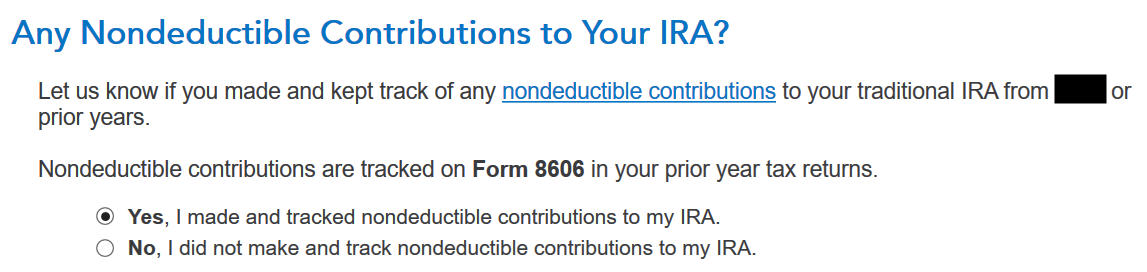

Foundation

Select “Sure” as a result of the 2022 Roth IRA contribution you recharacterized in 2023 counts as a nondeductible Conventional IRA contribution for 2022.

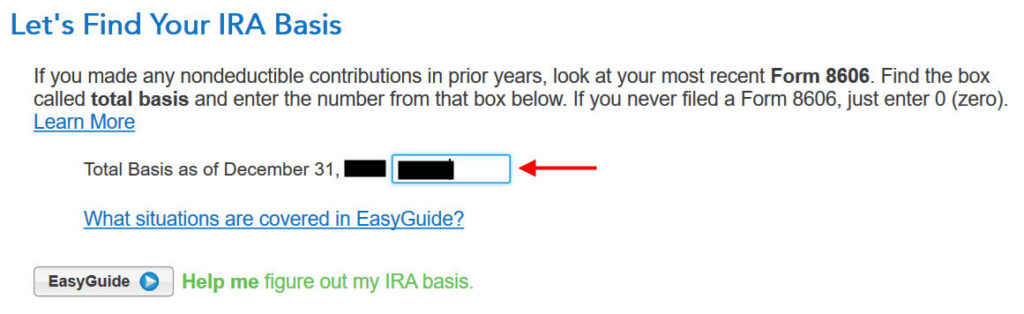

TurboTax ought to populate this worth from final 12 months’s return. If it doesn’t, get the worth out of your final 12 months’s Type 8606 Line 14, which you generated for those who adopted the earlier submit Backdoor Roth in TurboTax: Recharacterize and Convert, 1st Yr.

The refund meter goes again up after you enter the full foundation.

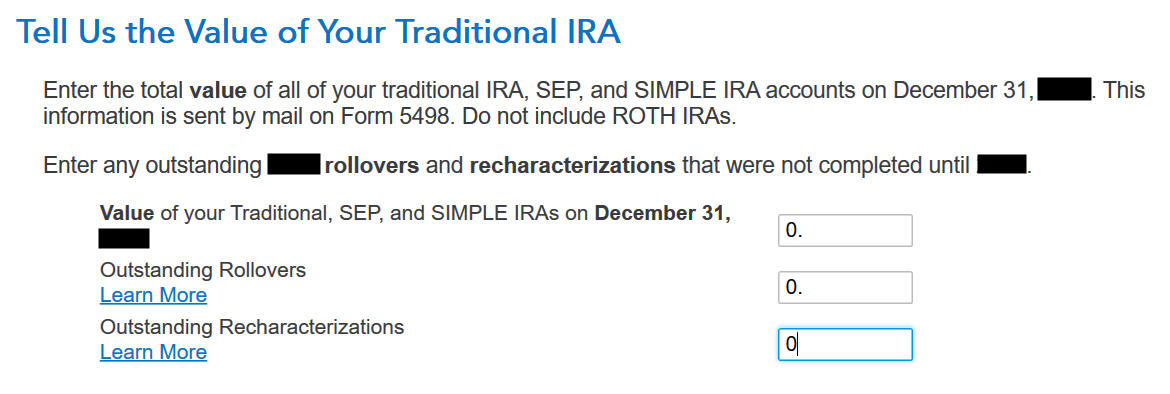

That is usually zero for those who transformed every little thing. In case you have just a few {dollars} left within the account from earnings posted after you transformed, enter the worth out of your year-end assertion within the first field.

Clear Conventional IRA Contribution

For those who additionally did a “clear” backdoor Roth in 2023 on prime of changing your contribution for 2022, in different phrases, you contributed to a Conventional IRA for 2023 in 2023 and transformed in 2023, your 1099-R contains changing two 12 months’s price of contributions in a single 12 months. All of the steps within the earlier part are nonetheless the identical besides that you’ve got a bigger quantity in your 1099-R kind.

The premise from the earlier 12 months’s tax return took care of one-half of the conversion. You additionally must report your 2023 Conventional IRA contribution. Please comply with the steps within the Non-Deductible Contribution to Conventional IRA part in our walkthrough for a clear backdoor Roth for 2023.

Say No To Administration Charges

In case you are paying an advisor a proportion of your property, you might be paying 5-10x an excessive amount of. Discover ways to discover an unbiased advisor, pay for recommendation, and solely the recommendation.

[ad_2]