[ad_1]

Think about the fun of shopping for that designer bag you have been eyeing, understanding you will not pay a dime further.

No bank card checks, no hidden charges – simply straightforward installments unfold over just a few weeks. That is the attraction of purchase now, pay later (BNPL) providers.

Removed from being simply one other development, BNPL is reshaping how shoppers method purchases, providing a compelling different to conventional credit score and debit transactions.

However earlier than you swipe, there is a essential query: is that this financing phenomenon only a fad or a recreation changer?

BNPL’s meteoric rise provides us front-row seats to the reshaping of how we pay. As we delve deeper into the BNPL phenomenon, it is important to grasp that its success will not be with out challenges. Issues about shopper debt, regulatory scrutiny, and the sustainability of the BNPL enterprise mannequin are important points that want addressing.

Nonetheless, these challenges additionally current alternatives for innovation, regulation, and schooling that may strengthen the BNPL sector and solidify its position in the way forward for shopper finance.

Evaluating the lifespan of purchase now pay later (BNPL) providers

Client Experiences signifies that BNPL packages elevated by 970% between 2019 and 2021. A “modest” $2 billion business immediately turned a juggernaut, producing $24.2 billion.

60%

of shoppers surveyed used a BNPL service through the COVID-19 pandemic, in search of to interrupt away from the standard credit score system.

This transition speaks volumes in regards to the altering panorama of shopper preferences. There may be rising disillusionment with typical credit score fashions and a robust need for extra adaptable and consumer-friendly monetary merchandise.

BNPL is a extra simple methodology of borrowing than conventional alternate options since credit score is prolonged with much less data.

In distinction to conventional shopper credit score, BNPL credit score is usually not communicated to credit score bureaus, that means no adversarial impact on the buyer’s credit score rating.

It differs from a layaway plan as a result of the patron receives the products or providers after paying the primary installment. In distinction, layaway plan consumers obtain them solely after paying the complete quantity.

Dividing a purchase order into interest-free installments is a large attraction, and shoppers can handle their bills whereas incurring small charges or none in any respect.

Supply: Juniper Analysis

Juniper says the substantial development of BNPL customers can be pushed by the anticipated financial downturn, which is able to improve the demand for low-cost credit score options.

The rising reputation of BNPL providers is pushed by a mix of things: the will for interest-free installment plans, the avoidance of conventional credit score rates of interest, and the attraction of a extra direct and manageable reimbursement construction.

The truth that BNPL has been extensively embraced suggests it fulfills a standard shopper need for monetary flexibility, one persisting regardless of financial shifts.

Moreover, the agility of BNPL suppliers in responding to shopper wants, evolving financial situations, and regulatory landscapes has been pivotal in sustaining this development.

Lovers use BNPL (also referred to as point-of-sale installment loans) to juggle their budgets to buy clothes, tech devices, and residential furnishings. It’s seen by many as a lifesaver in a turbulent monetary time. Others view it as a system that, when misused, is an invite so as to add extra debt.

The professionals of BNPL are the flexibility to make funds in installments. Shoppers routinely elect to pay 25% upfront after which 25% throughout two-, four-, and six-week intervals to cowl the remaining steadiness. This permits higher cash administration and hopefully extra management over spending habits.

This turns into particularly essential when buying big-ticket gadgets, because the prolonged timeframe provides consumers ample time to replenish financial institution accounts earlier than the following scheduled cost.

The prolonged cost plan is interesting, and a few shoppers could also be inclined to ultimately exchange their bank card with the interest-free possibility supplied by BNPL.

Finest practices for accountable BNPL providers use

To harness the advantages of BNPL whereas mitigating monetary pressure dangers, shoppers and suppliers should undertake a conscientious method.

Listed below are concrete suggestions for the accountable and sustainable use of BNPL providers:

Set clear budgeting pointers

Shoppers ought to assess their monetary state of affairs earlier than utilizing BNPL providers. Establishing a finances that accounts for BNPL funds can forestall overspending.

It is essential to contemplate not simply the attract of speedy buy however the dedication to future funds.

Perceive the phrases totally

Earlier than agreeing to a BNPL plan, it is important to completely perceive the phrases and situations. This consists of any charges for late funds, the cost schedule, and the impression (if any) on credit score scores.

Clear comprehension of those points can forestall sudden monetary burdens.

Use BNPL for mandatory purchases solely

Whereas BNPL may be tempting for every type of purchases, prioritizing important or important investments over impulsive buys can improve monetary wellness.

This strategic method ensures that BNPL serves as a instrument for monetary administration relatively than a supply of avoidable debt.

Monitor BNPL commitments

Retaining monitor of all BNPL plans is important to keep away from overcommitting financially. Shoppers ought to think about using monetary administration apps or instruments that consolidate all BNPL obligations in a single place, providing a transparent view of upcoming funds and complete indebtedness.

Emergency financial savings over BNPL

Each time potential, shoppers ought to purpose to construct an emergency financial savings fund that can be utilized for sudden bills relatively than counting on BNPL.

This proactive monetary behavior can scale back the necessity for deferred cost providers and contribute to general monetary stability.

BNPL suppliers’ position in selling duty

Suppliers ought to supply clear, user-friendly details about their providers, together with clear disclosures of charges and fees.

Offering instructional assets on monetary literacy and accountable spending, together with instruments for finances administration and cost monitoring, can empower shoppers to make use of BNPL correctly.

Encourage early cost choices

BNPL providers that reward early reimbursement or supply versatile cost schedules encourage accountable use. Such choices may help shoppers handle their funds extra successfully and keep away from debt accumulation.

Regulatory compliance and finest practices

BNPL suppliers ought to adhere to regulatory requirements and finest practices, making certain shopper safety is on the forefront of their operations.

This consists of conducting affordability checks earlier than providing providers to scale back the danger of lending to shoppers who might wrestle to satisfy reimbursement obligations.

By following these pointers, BNPL providers may be utilized as a accountable monetary instrument that advantages shoppers by offering flexibility and management over their spending whereas additionally making certain that this revolutionary cost possibility stays sustainable and viable in the long run.

The evolution of BNPL providers within the shopper market

The BNPL enterprise mannequin started in Europe and Australia and gained momentum a couple of decade in the past. Its attraction gained traction with the rise of e-commerce through the COVID-19 pandemic.

BNPL turned a well-liked manner to purchase garments and residential furnishings with shoppers homebound and flush with money.

With hovering inflation, the next value of residing, and skyrocketing rates of interest on bank cards, many patrons now flip to BNPL providers to make on a regular basis purchases.

These elements have a ripple impact on the next:

- Client conduct: When rates of interest improve, shoppers change into extra cost-conscious and hesitant to tackle further debt.

This leads them to hunt choices that supply decrease upfront prices than conventional bank cards with excessive rates of interest. - Value of borrowing: When the broader financial system’s rates of interest rise, the price of borrowing throughout the board additionally will increase. Because of this, some BNPL suppliers might cost charges to shoppers who decide to unfold out funds.

- Competitors: The BNPL business is very aggressive, and market share is all the things to suppliers. As rates of interest rise, the dynamics throughout the BNPL sector will change.

Some suppliers might regulate pricing and phrases to stay aggressive, whereas others might give attention to effectivity and value financial savings to retain shopper attraction.

A number one advocacy and commerce affiliation, Digital Transactions Affiliation (ETA), reported a 30% BNPL penetration for Gen Z and millennials in 2021, which is anticipated to rise to 40% by 2025.

The affiliation says that whereas solely 6% of child boomers selected BNPL, that quantity is projected to be as excessive as 15% by 2025. Gen Z and millennials are 55% extra doubtless than different generations to make use of BNPL.

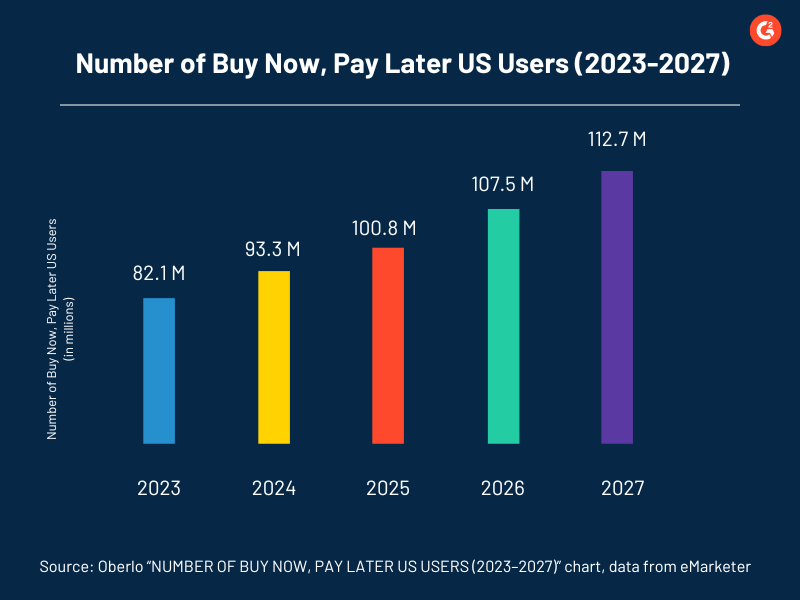

Within the face of rising prices, shopper spending utilizing BNPL providers is estimated to extend 290% by 2027, which implies $437 billion can be spent on items worldwide.

In response to Investopedia, Gen Z has the bottom credit score scores of all generations as a result of proudly owning fewer bank cards (a median of two). This information may be beneficial for establishments with a longtime older member buyer base.

Supply: Oberlo

Enterprise house owners who acknowledge the worth of BNPL are fast to leap on board as a result of they consider shoppers can be enticed to spend extra and full the sale.

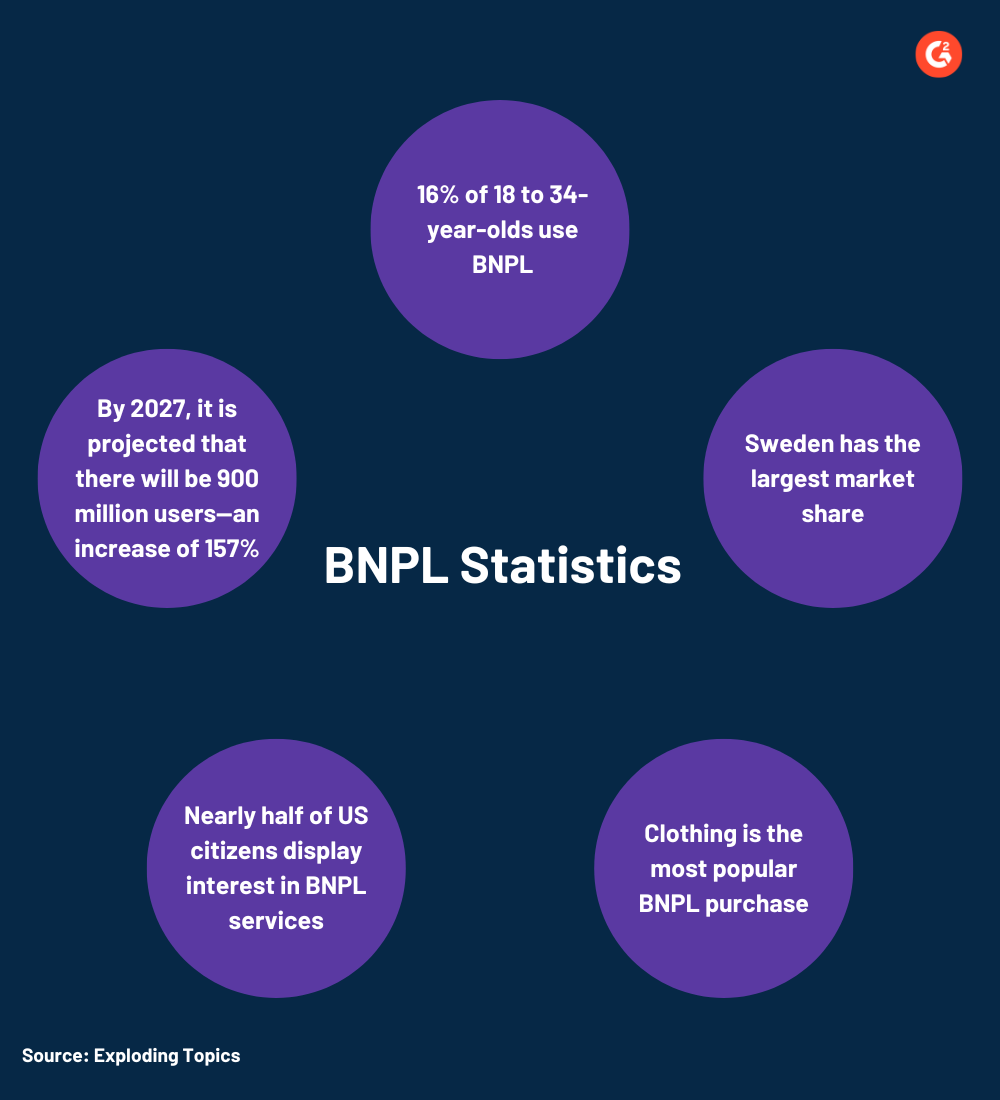

At present, in line with Exploding Matters, there are about 360 million BNPL customers worldwide, and that market is value greater than $150 billion.

Supply: Exploding Matters

Purchase now, pay later vs. bank cards

BNPL providers current a compelling different to conventional credit score mechanisms. Bank cards supply the pliability of minimal month-to-month funds and advantages akin to rewards factors and cashback, options not generally present in BNPL providers.

Nonetheless, the necessity for arduous credit score checks and the danger of excessive curiosity on balances might make bank cards much less accessible for some.

Benefits of BNPL providers over bank cards embrace:

- Versatile cost plans: BNPL providers allow clients to distribute the price of their purchases over a number of installments, easing finances administration with out speedy monetary pressure.

- Ease of entry: By forgoing arduous credit score checks, BNPL options open doorways for a broader spectrum of shoppers, together with those that might not qualify for typical credit score choices.

- Environment friendly approval processes: With notably excessive approval charges, particularly amongst youthful demographics, BNPL gives a sensible resolution for these needing swift monetary flexibility.

- Curiosity-free preparations: Probably the most interesting points of BNPL plans is their lack of curiosity fees, contrasting with the potential for accruing curiosity on bank card balances.

- Renewable credit score choices: As repayments are accomplished, credit score availability is promptly restored, empowering shoppers to make future purchases responsibly.

Nonetheless, some challenges and areas with room for enchancment embrace:

- Payment transparency: It is important for customers to completely perceive any charges related to late funds or service fees. Striving for utmost funds successfully.

- Lack of rewards and shopper protections: Conventional rewards and protections supplied by bank cards are areas the place BNPL providers usually fall brief. Improvements are underway to bridge this hole, enhancing the worth and safety of BNPL transactions.

Recognizing the worth of shopper safety options inherent to bank cards, there’s an ongoing effort to include related safeguards inside BNPL providers, making certain a safe and useful person expertise.

Whereas acknowledging the strengths of conventional bank cards, the distinctive advantages of BNPL — together with its accessibility, budget-friendly cost choices, and lack of curiosity fees — place it as a necessary instrument within the monetary toolkit of latest shoppers.

Trying forward, the main focus can be on enhancing the BNPL mannequin via elevated transparency, educating clients about its advantages, and introducing further benefits.

This can purpose to attain a harmonious steadiness between the revolutionary attraction of BNPL and the established advantages of bank cards.

Challenges to BNPL providers

As BNPL providers broaden, they face rising scrutiny and challenges round rates of interest, laws, and shopper dangers.

There aren’t any rate of interest fees and no arduous credit score checks in a typical BNPL platform. This will increase e-commerce conversion and opens the chance for extra repeat purchases. It is essential to fastidiously weigh these advantages in opposition to potential downsides.

One draw back is that customers forfeit conventional bank card perks, akin to rewards factors and buy safety (though the counterbalance is a zero rate of interest and extra management over money circulation).

Nonetheless, the danger of overspending as a result of installment funds is a major concern. Impulse shopping for is an actual chance, and those that do not pay on time might accumulate late charges, doubtlessly damaging their credit score scores.

Moreover, BNPL platforms usually have limits on the quantity that may be financed, which might not be appropriate for bigger purchases.

Whereas BNPL may be an asset for people who have to handle their money circulation, it isn’t with out potential issues. Though purchases usually do not straight have an effect on a credit score rating, late or missed funds on BNPL could also be reported to third-party bureaus and will increase considerations about one’s capacity to satisfy mortgage necessities.

On this situation, a lender might require the client to scale back, repay, or shut their BNPL service. It is also essential to notice that some BNPL suppliers cost charges, doubtlessly rising the overall buy value in comparison with conventional strategies.

So, is BNPL sustainable over the long run?

BNPL’s success relies on adapting to market modifications and laws and prioritizing shopper well-being.

Navigating these challenges via monetary literacy, accountable regulatory innovation, and shopper safety is essential for BNPL suppliers to stay a beneficial and sustainable monetary instrument for various shoppers.

OCC’s pointers for managing BNPL dangers

Cooley’s experiences spotlight the Workplace of the Comptroller of Forex’s (OCC) steering to banks on managing BNPL threat.

The rules warn of potential “credit score, compliance, operational, strategic, and fame dangers” for shoppers and banks, significantly for short-term, no-interest loans repayable in 4 installments or much less.

Key dangers for debtors embrace overextension, further charges, and difficulties with returns. Banks face challenges as a result of restricted visibility into debtors’ full monetary obligations and the potential for operational and compliance dangers when counting on third-party BNPL suppliers.

The OCC emphasizes continued regulatory give attention to BNPL, urging all events to evaluate insurance policies and procedures for compliance and anticipate potential further federal laws.

Rising rates of interest add additional dangers

Along with regulatory scrutiny, rising rates of interest pose one other problem for BNPL providers. Greater borrowing prices might result in extra missed funds and defaults, particularly amongst financially susceptible shoppers.

Some BNPL suppliers now supply longer-term loans with rates of interest as excessive as 36%, exceeding many bank cards.

Client advocates advocate guardrails, akin to checking for excellent debt earlier than approving BNPL and suspending the choice for past-due clients. Retailers must also assist laws selling accountable practices.

Monitoring the impression of rising charges on delinquencies, significantly for longer-term, higher-interest BNPL merchandise, is essential.

The evolving debates round BNPL regulation and rising rates of interest underscore the necessity for vigilance and a balanced method.

As shopper demand grows, BNPL suppliers, monetary establishments, regulators, and retailers should collaborate to foster accountable innovation that prioritizes shopper safety and monetary well-being.

Developments, expertise, and improvements to deal with BNPL’s shortfall

Comfort prompts shoppers to make use of BNPL.

Longer to pay, cheaper, easier, and pace all match into BNPL’s wheelhouse. However the financial ache of excessive rates of interest and inflation as a driver for different credit score options can’t be discounted. Youthful shoppers who span a number of revenue brackets embrace BNPL and use it for informal spending and to handle their cash higher.

The Federal Reserve Financial institution of Philadelphia says that the heaviest customers of BNPL providers within the U.S. are households with common incomes above $75,000.

These with an revenue of lower than $40,000 are much less doubtless to make use of the service. The acquisition of garments is the highest product financed, adopted by electronics, footwear, residence décor, and equipment.

The business most impacted is e-commerce, which grew through the pandemic. Rising curiosity, inflation, and different elements have stalled its development. In response to similarweb.com, retailers face a really aggressive enjoying subject and will look to developments, tech, and innovation to make up for the shortfall.

In response to their report, the electronics business hit arduous final yr, with visits and conversions down throughout the board. But, in its survey, 26.7% of shoppers used BNPL to purchase electronics they might not have in any other case been capable of buy with out utilizing BNPL.

Retailers can embrace a number of methods to revive BNPL utilization and broaden its functions:

Personalization and AI

Implementing AI to personalize procuring experiences and BNPL gives can improve shopper engagement.

By analyzing shopper conduct, retailers can tailor their BNPL choices to match particular person preferences and monetary capabilities, making purchases extra interesting and manageable.

Integration of monetary schooling

Integrating instructional instruments throughout the BNPL course of may help shoppers make knowledgeable selections.

Offering insights on finances administration, rates of interest, and the long-term implications of BNPL can foster a extra accountable and knowledgeable shopper base.

Seamless omnichannel experiences

Enhancing the BNPL expertise throughout all retail channels can handle the e-commerce development stall.

By providing BNPL each on-line and in-store, retailers can create a seamless omnichannel procuring expertise that encourages extra frequent use of BNPL providers.

Growth of BNPL use circumstances

Broadening the scope of BNPL past conventional retail to incorporate providers akin to healthcare, schooling, and journey might open new markets. This enlargement can drive development by making BNPL a ubiquitous a part of bigger monetary selections, not simply retail purchases.

Partnerships and collaborations

Forming strategic partnerships between BNPL suppliers and monetary establishments might introduce new merchandise that mix the advantages of bank cards (e.g., rewards packages) with the pliability of BNPL.

Such collaborations might additionally improve shopper safety and belief in BNPL providers.

Sustainability and moral concerns

As shoppers change into extra conscious of their environmental impression, BNPL providers want to include sustainability and moral concerns of their choices. This may help differentiate their providers from others out there.

By incentivizing clients to buy environmentally pleasant merchandise or from socially accountable firms, BNPL suppliers can align themselves with the broader shopper values.

BNPL is the daybreak of a brand new monetary period

BNPL isn’t just a passing craze however a recreation changer for the way forward for finance.

This conviction is rooted in observing BNPL’s speedy adoption charges and its capacity to deal with the speedy wants of a various shopper base. By providing extra flexibility than conventional credit score techniques, BNPL providers are democratizing entry to monetary instruments for a broad spectrum of shoppers.

There at the moment are conversations about diversification in cost choices inside BNPL providers and a redefinition of BNPL procuring requirements.

Advances in monetary expertise are resulting in the integration of functionalities akin to the flexibility to make funds by textual content message. Comfort is commonly the important thing to profitable gross sales, and BNPL choices supply simply that to clients.

We at the moment are in a contactless enterprise setting.

Shoppers get pleasure from the advantages of BNPL and might unfold out their purchases over time whereas paying swiftly by textual content as an possibility. BNPL is yet one more tech development that’s secure and quick and places energy in a shopper’s hand.

BNPL is evolving, and its future appears very vivid.

Study how one can attain the following technology of Gen Z shoppers and form the way forward for your model.

Edited by Shanti S Nair

[ad_2]